How Sustainability Rewrites the Cost of Capital

How Sustainability Rewrites the Cost of Capital

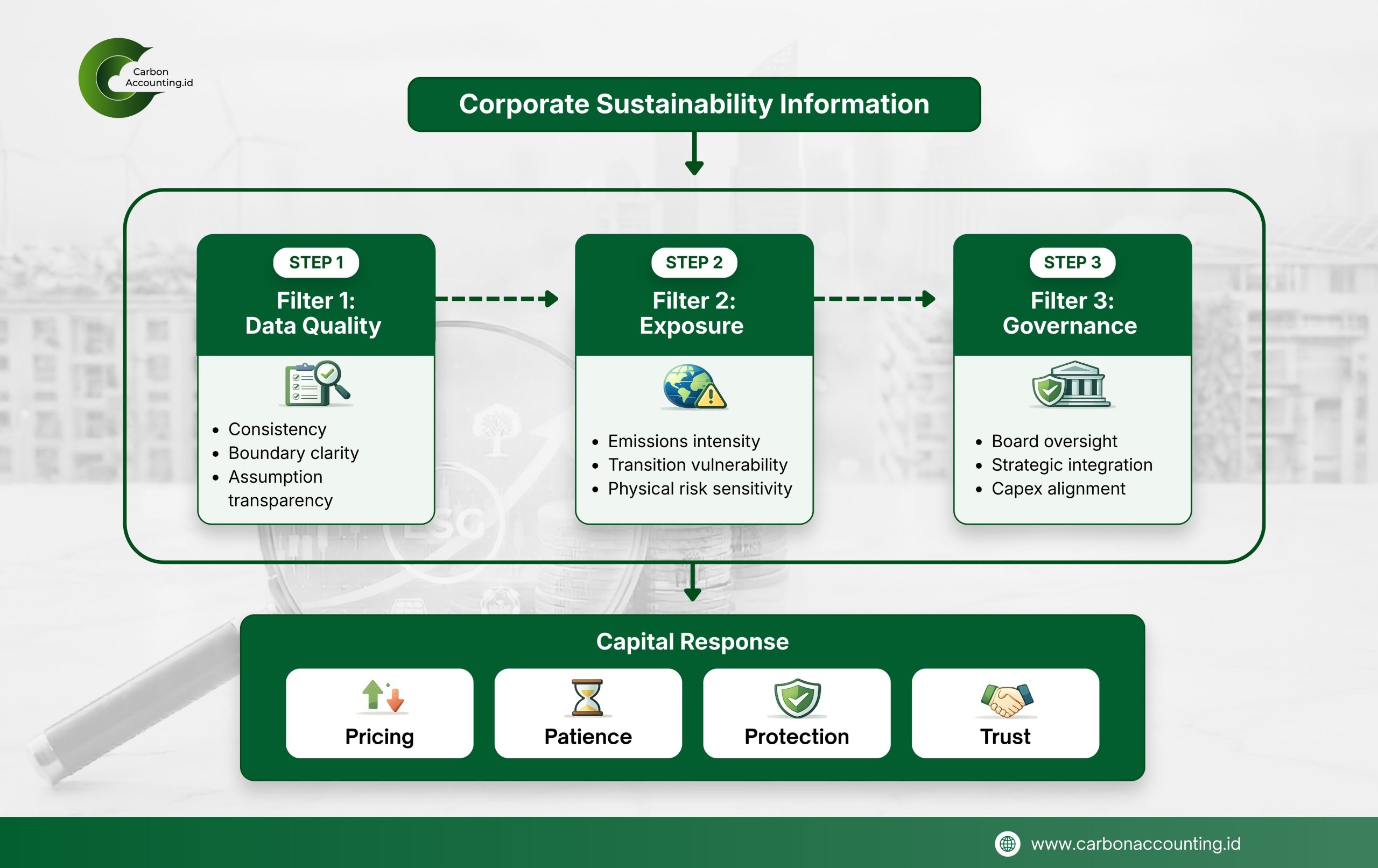

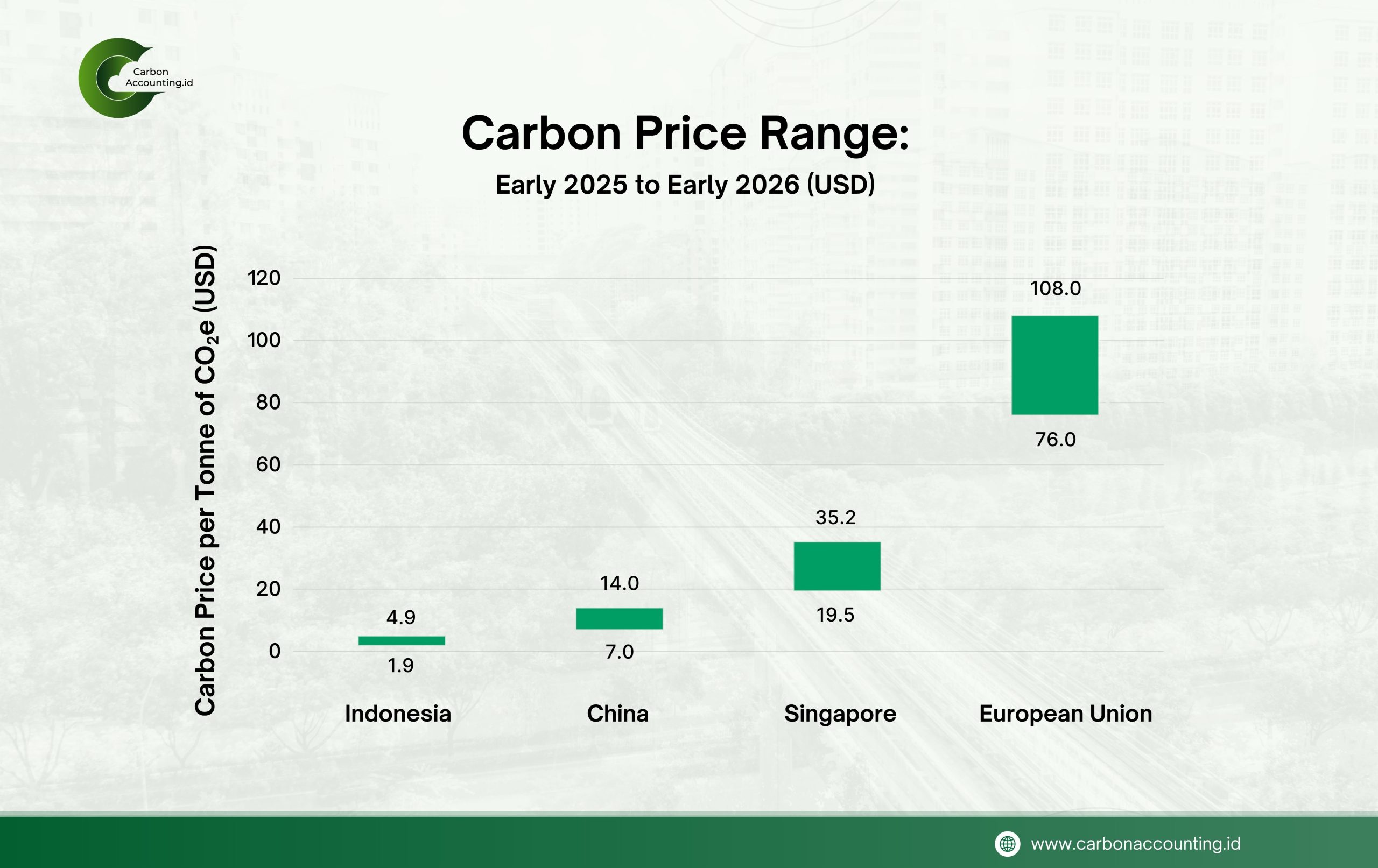

The Three Filters Before Capital Responds: How Sustainability Information is Translated into Market Judgment.

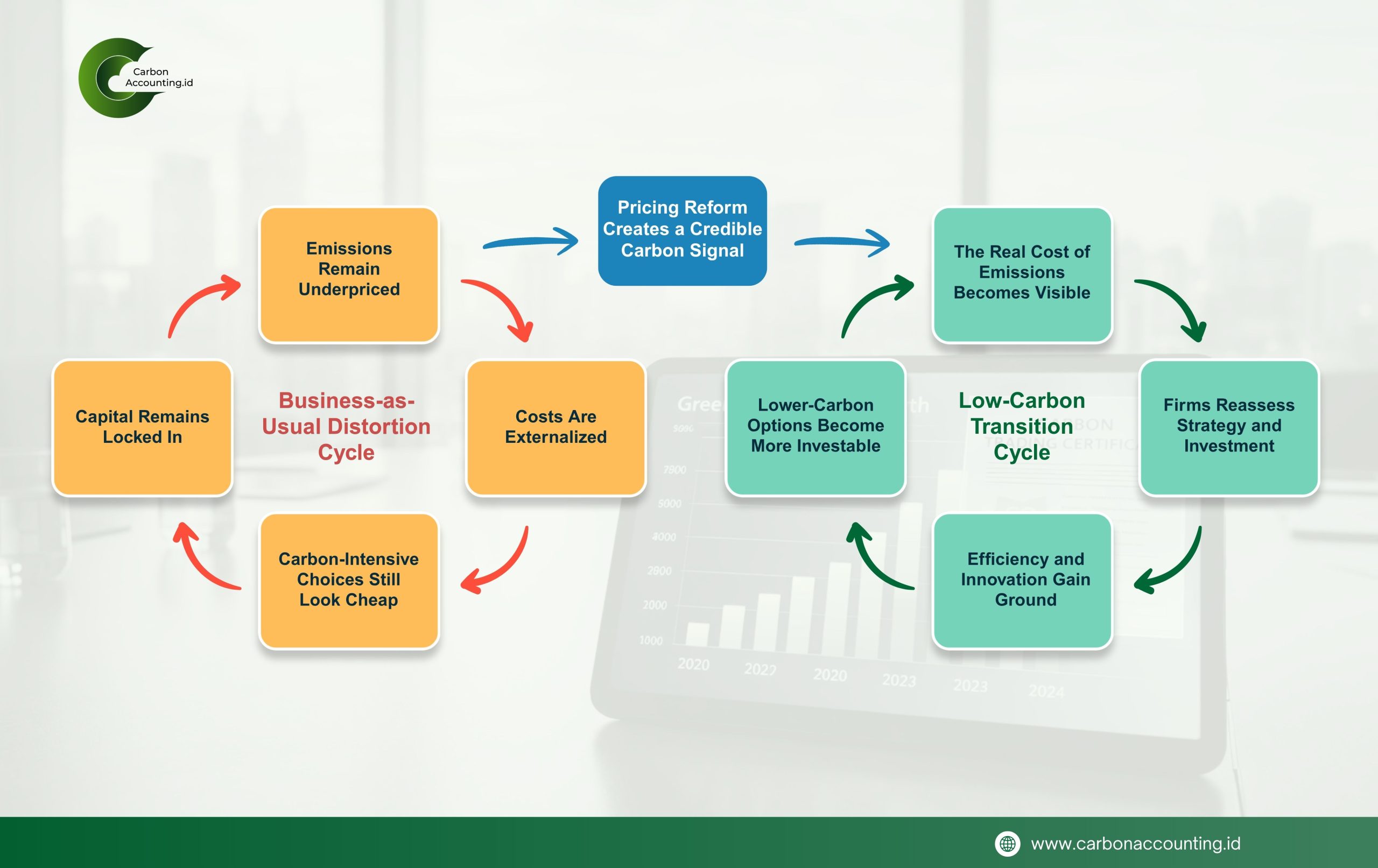

The market has a cold way of expressing doubt. It does not shout. It widens the spread, shortens the tenor, tightens the covenant, and leaves the company to discover that sustainability has started to enter the price.

This is the point where disclosure stops sitting quietly in the report and starts affecting financial decisions. Once lenders and investors can see a company’s emissions profile, transition exposure, governance, and the strength of its targets more clearly, sustainability begins to influence how that company is judged, priced, and trusted.

The first filter is data quality. Weak data creates doubt, and doubt is expensive. When emissions numbers are inconsistent, assumptions are unclear, or the scope of reporting keeps shifting, creditors and investors begin to treat the company itself as harder to read. The result is often caution, and caution has a cost.

The second filter is exposure. High emissions alone do not necessarily close the market’s door. What makes investors uneasy is high emissions without a believable transition path. More and more, the market is learning to separate real progress from polished claims. Once that difference becomes visible, it can affect financing, valuation, and trust.

Governance matters just as much. If sustainability sits outside strategy, outside capex, and outside board attention, the market reads that as fragility. Good governance does not guarantee cheap capital, but it can reduce uncertainty. And in finance, uncertainty is often what turns into a premium.

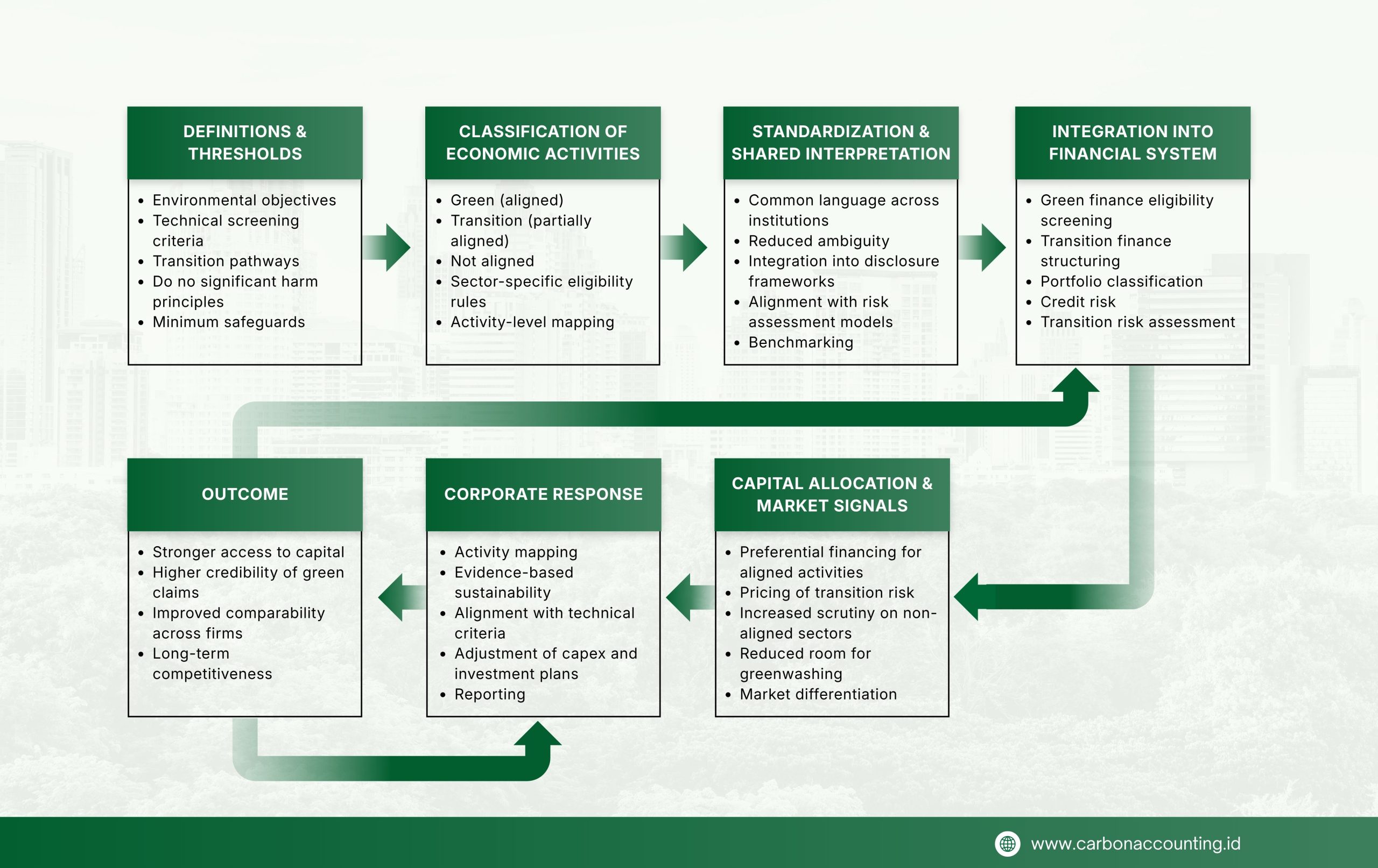

This is why the IFRS S2 amendments matter beyond compliance. They push disclosure toward clearer boundaries and more decision useful information, especially in the financial sector. As banks, investors, and asset managers improve the way they read climate related data, the quality of corporate sustainability information will matter more directly in credit analysis, portfolio selection, and engagement.

For the wider business community, the consequence is clear. Sustainability now reaches beyond reputation and regulation. It begins to affect whether capital feels secure, whether it remains patient, and whether the market sees the company as worth backing over time.

That is the deeper rewrite now underway. Sustainability does not change the cost of capital in one dramatic moment. It changes it quietly, through risk perception, confidence, and comparability. And once that happens, the question is no longer whether sustainability matters to finance, but how much a company will pay when it fails to matter enough.

{kind=link}

{kind=link}

{kind=link}

{kind=link}