Indonesia’s Carbon Price Problem: A Market Too Weak to Matter

Indonesia’s Carbon Price Problem: A Market Too Weak to Matter

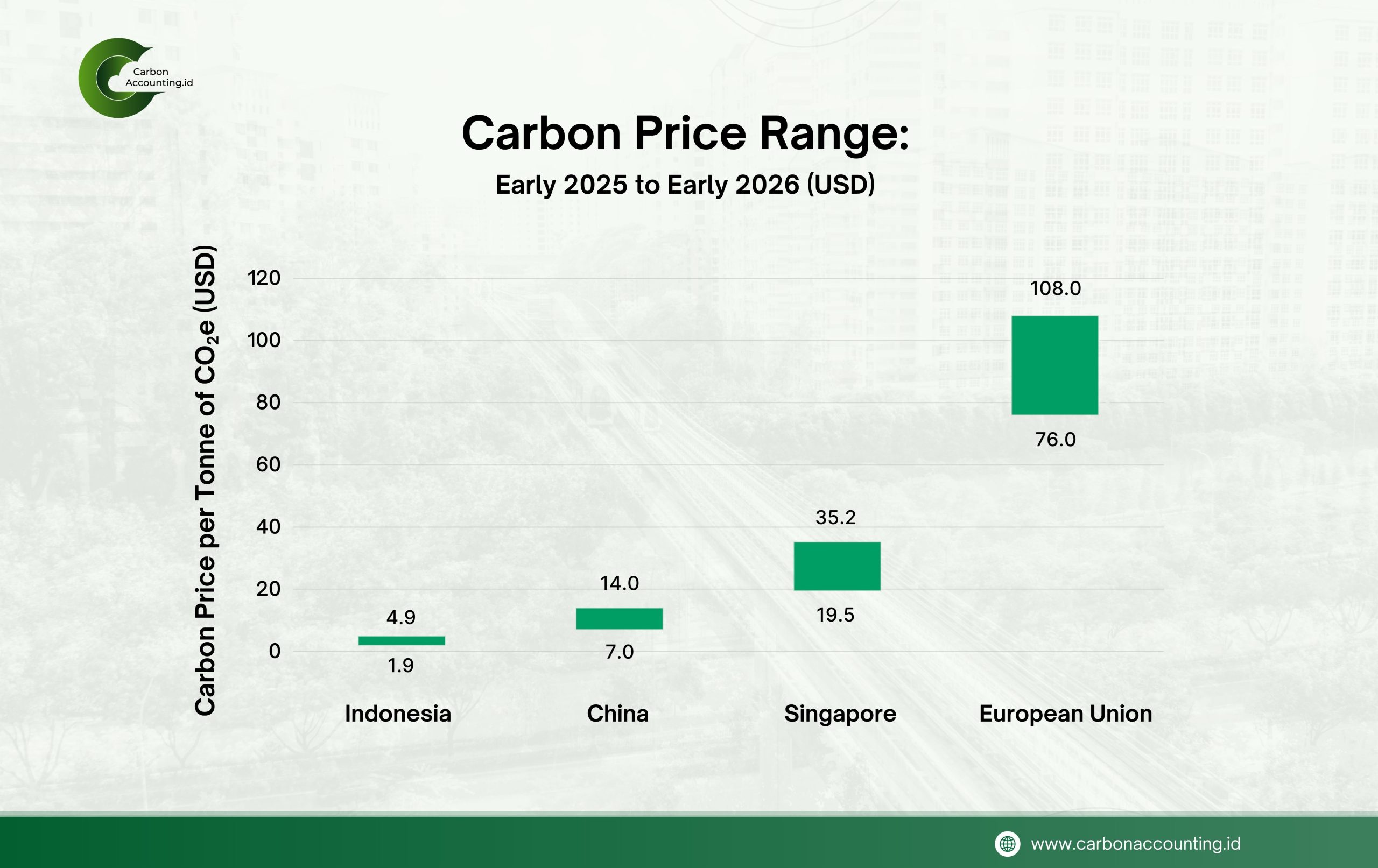

Comparison of Carbon Price Ranges: Indonesia, China, Singapore, and the European Union

A carbon price becomes real only when it can interrupt habit. Until it can alter fuel choices, technology choices, and investment plans, it remains louder in policy speeches than in boardrooms.

That is the oldest weakness of carbon pricing. A price may exist on paper and still feel too small to disturb business as usual. When coverage is narrow, permits are generous, compliance is light, and trading is thin, carbon is absorbed as a routine expense, not read as a strategic signal.

This matters because weak prices do more than disappoint. They teach the market the wrong lesson. The World Bank notes that carbon pricing now reaches about 28 percent of global emissions. But only a limited portion is priced at levels widely seen as strong enough to drive change. The issue is no longer simply whether carbon pricing exists, but whether it carries real economic weight.

Indonesia shows this problem clearly. The country already has a compliance ETS, but it is still centred on the power sector. Based on reported transaction values and volumes on IDXCarbon from early 2025 to early 2026, the observed price range was only about USD 1.9 to USD 4.9 per tCO2e. The market exists, but the signal is still faint.

The contrast is hard to miss. Over roughly the same period, the EU ETS moved at about USD 76.0 to USD 108.0 per tCO2e. China’s national ETS sat in a much lower but still firmer band of roughly USD 7.0 to USD 14.0. Singapore used a different instrument altogether, with a statutory carbon tax of S$25 in 2025 and S$45 in 2026, or about USD 19.5 to USD 35.2.

Seen against the often-cited benchmark of USD 50 to USD 100 by 2030, Indonesia still looks much closer to an opening signal than to a price capable of reshaping technology choice and capital allocation.

That does not mean carbon pricing is irrelevant. It means that pricing without sufficient strength risks becoming a symbol of transition rather than a driver of it. A market can look alive long before it becomes persuasive.

In the end, a carbon market proves itself not when it starts trading, but when delay becomes more expensive than action.

{kind=link}

{kind=link}

{kind=link}

{kind=link}