Why Good Climate Projects Still Struggle to Find Capital

Why Good Climate Projects Still Struggle to Find Capital

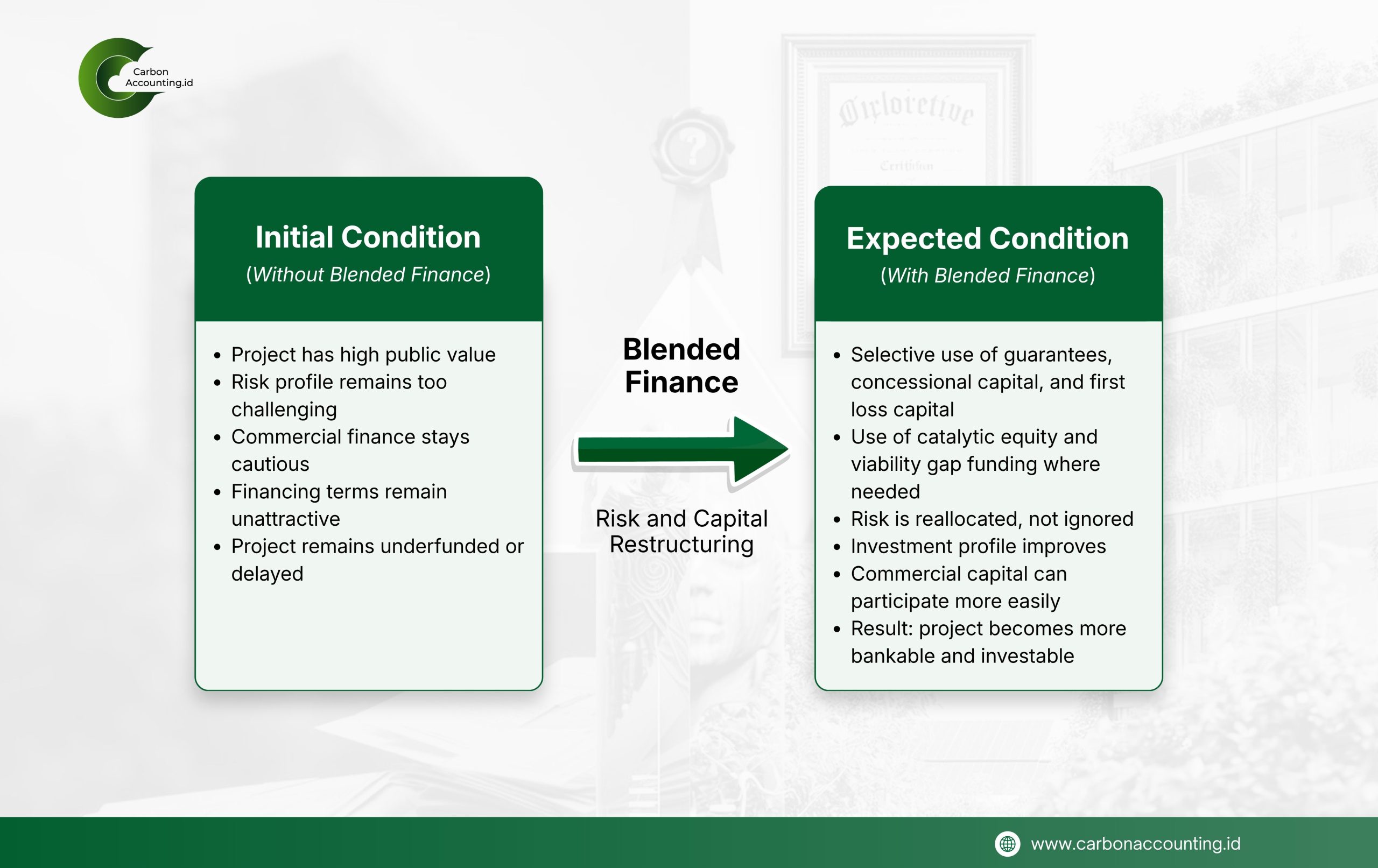

From Public Value to Bankability: The Role of Blended Finance

Capital does not stay away because a project lacks value. More often, it stays away because the risk is arranged badly.

That is why many transition and adaptation projects in Indonesia still struggle to become bankable when they rely only on conventional commercial finance. In emerging and developing economies, high perceived risk keeps the cost of capital elevated, even when the public value is obvious.

Blended finance begins to matter when it stops sounding virtuous and starts changing the deal. Its purpose is to rearrange capital and risk so commercial investors can enter projects they would otherwise avoid. The real question is no longer whether a project matters, but what design can make it investable.

Guarantees are often the turning point in a difficult financing structure. Their role is to take on risks that private lenders cannot price with confidence or do not want to carry by themselves. That change can improve financing terms, extend maturities, and help a borrower move from doubtful to investable.

Concessional capital plays a different role. Used well, it does not replace markets. It prepares them. It can absorb specific risks, help create markets, and reduce the cost of capital for projects with strong public value but weak commercial appeal.

First loss structures and catalytic equity matter for the same reason. When public or philanthropic capital takes the earliest shock, senior investors gain protection that can make participation possible. What matters is not only how much support is offered, but where that support sits in the capital stack.

Some projects need one more bridge, namely viability gap funding. Where revenues are too weak or too delayed to cover efficient project costs, grant support can close the gap. But discipline still matters. Blended structures should address genuine market failure, not subsidize deals private finance would have funded anyway.

Adaptation tells the story plainly. Between 2016 and 2021, public interventions mobilized only USD 7.1 billion of private finance for adaptation, against USD 69.5 billion for mitigation. The message is hard to miss. Resilience projects usually need guarantees, concessional capital, and public risk sharing before private money is willing to come alongside.

After the cooling of sustainability linked finance hype, the real contest is no longer about who can tell the greenest story. It is about who can build a structure strong enough to carry difficult projects into the market without losing discipline.

{kind=link}

{kind=link}

{kind=link}

{kind=link}