Climate Physical Risks v1.2

Climate Physical Risks v1.2

There is a reason climate risk feels different now. Floods can silence a factory in a day, and heat can sap momentum across an entire quarter. What used to sound like a future cost is showing up as a current crisis. The horizon is not coming. It is already beneath our feet.

The strongest impetus comes from reporting frameworks. The TCFD frames climate related disclosure across governance, strategy, risk management, and metrics and targets. IFRS S2 sets a disclosure baseline that requires companies to explain physical and transition risks consistently. In Indonesia, PSPK 2 is aligned with this baseline and becomes effective for reporting periods beginning 1 January 2027, making physical risk a core part of reporting.

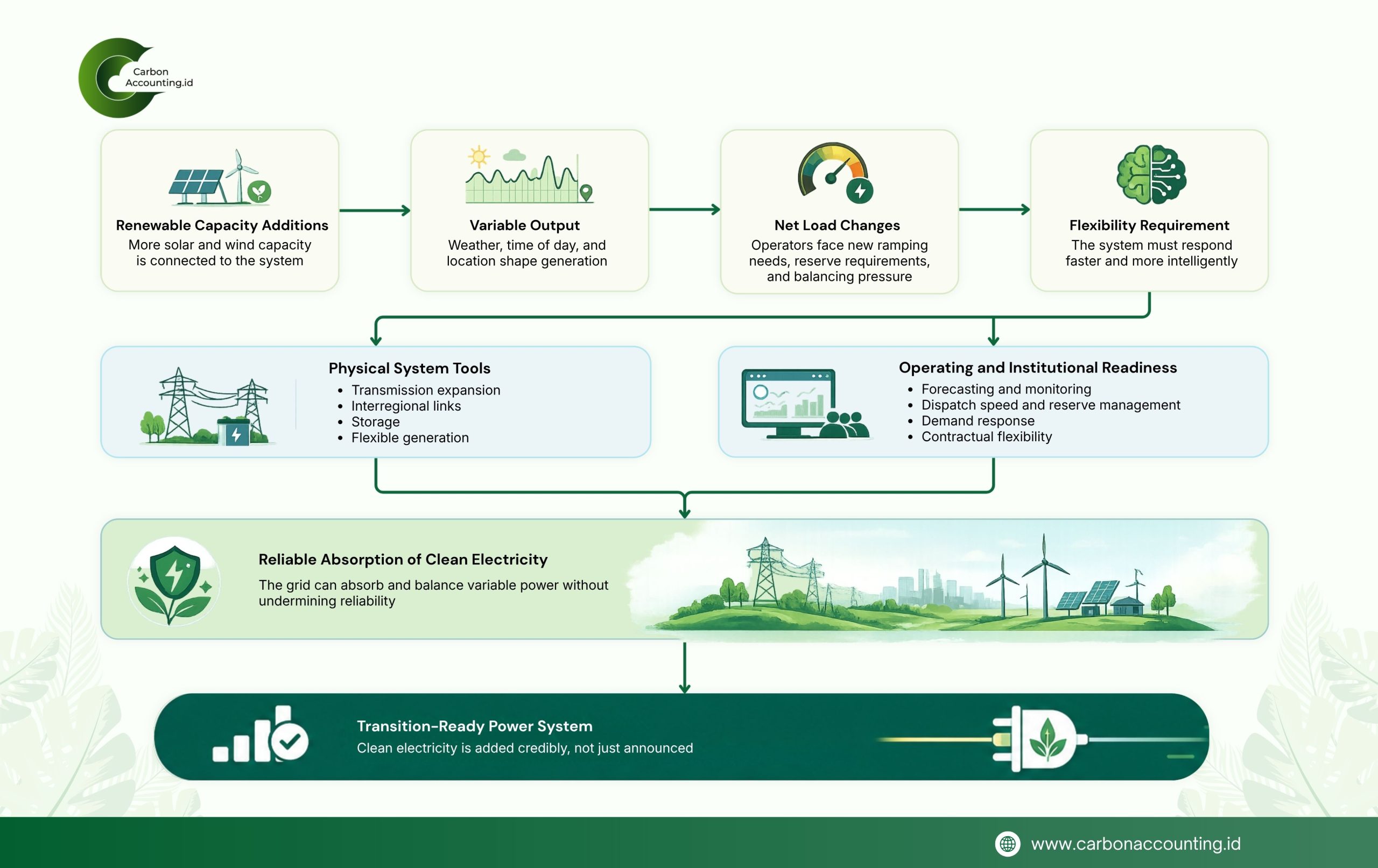

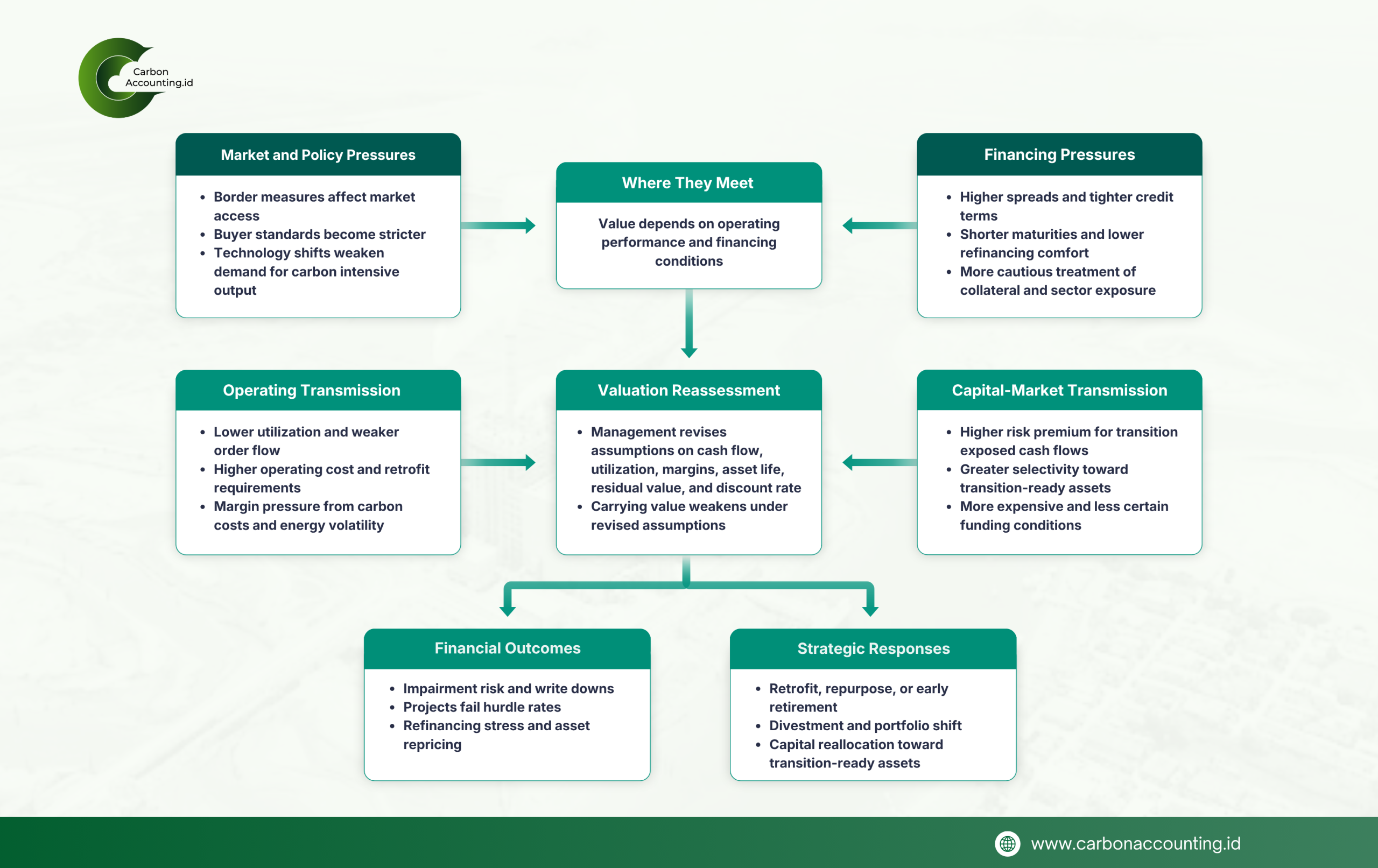

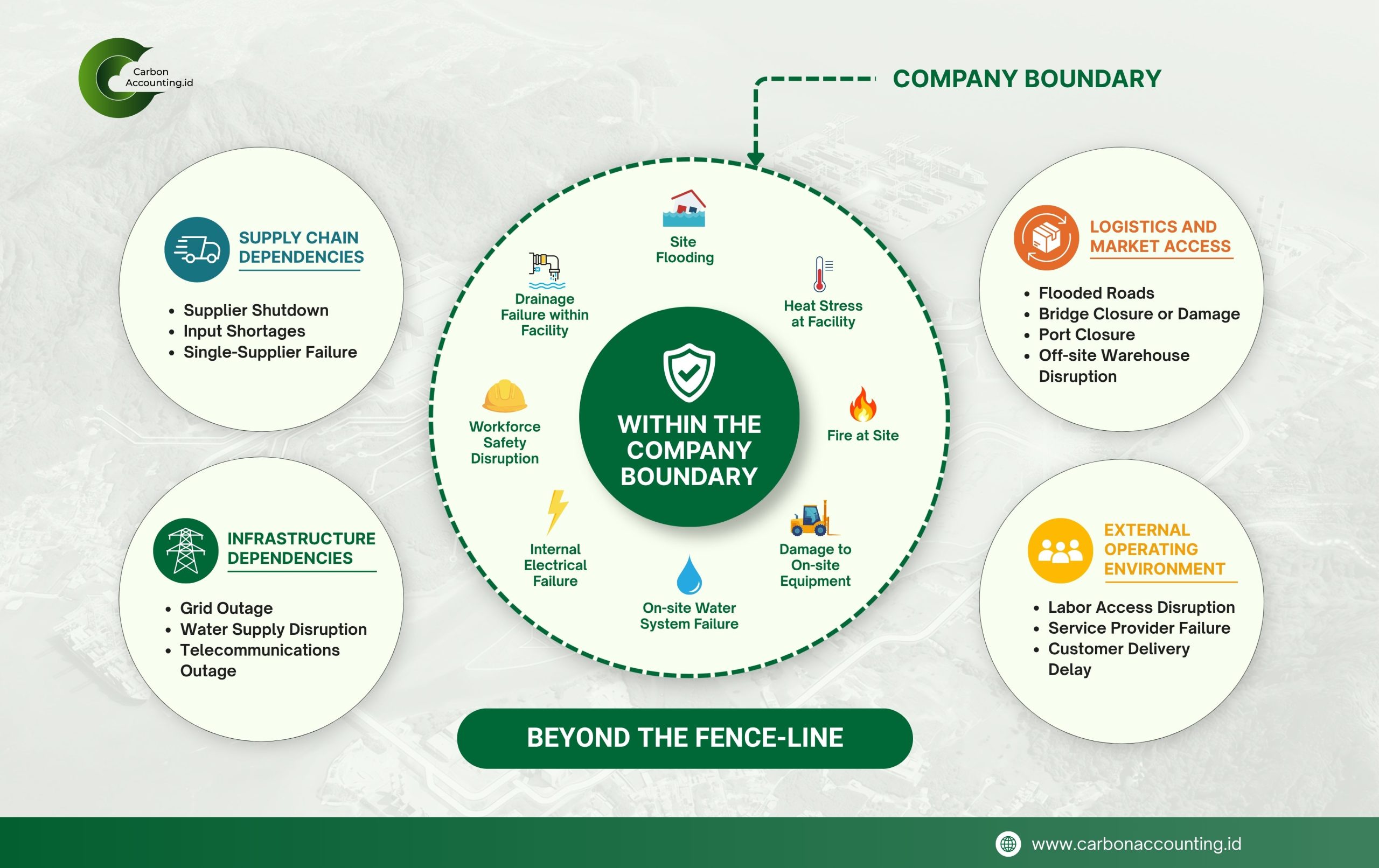

Conceptually, climate related physical risks are risks resulting from climate change that affect assets, operations, people, and supply chains. They are usually grouped into acute risks and chronic risks.

Acute risks are event driven climate hazards that arrive quickly and cause disruption right away, such as heavy rainfall, floods, storms, droughts, heatwaves, and forest fires. They tend to translate into practical problems, stopped operations, damaged assets, delayed deliveries, and higher operating costs.

Chronic risks move more slowly, but they shift the baseline of performance. Rising average temperatures increase cooling loads and raise heat stress for workers. In coastal areas, risks often stack together as a reinforcing chain.

At CarbonAccounting.id, the Climate Physical Risks v1.2 helps companies map physical risks in language that works for risk teams and auditors. For chronic risks, we assess temperature risk and integrated coastal risks, covering sea level rise, land subsidence, tidal risk, and wave risk. For acute risks, we assess rainstorm risk, drought risk, and wildfire risk, then translate them into what they mean for sites and continuity plans.

Anchored in high resolution geospatial data and a suite of climate models, our service documents data sources, assumptions, and key inputs so the results can be reviewed and used confidently in disclosure. The end result is a practical summary that can feed strategy narratives, risk registers, and metrics expected under TCFD and IFRS S2, aligned with PSPK 2.

Beyond the ledger, we weave resilience into an earth that has already changed. If you would like to develop a physical risk analysis in accordance with IFRS S2, our team is ready to discuss. Precision is the compass as climate risk becomes a presence.

{kind=link}

{kind=link}

{kind=link}

{kind=link}