When High-Carbon Assets Start Losing Value Before They Shut Down

When High-Carbon Assets Start Losing Value Before They Shut Down

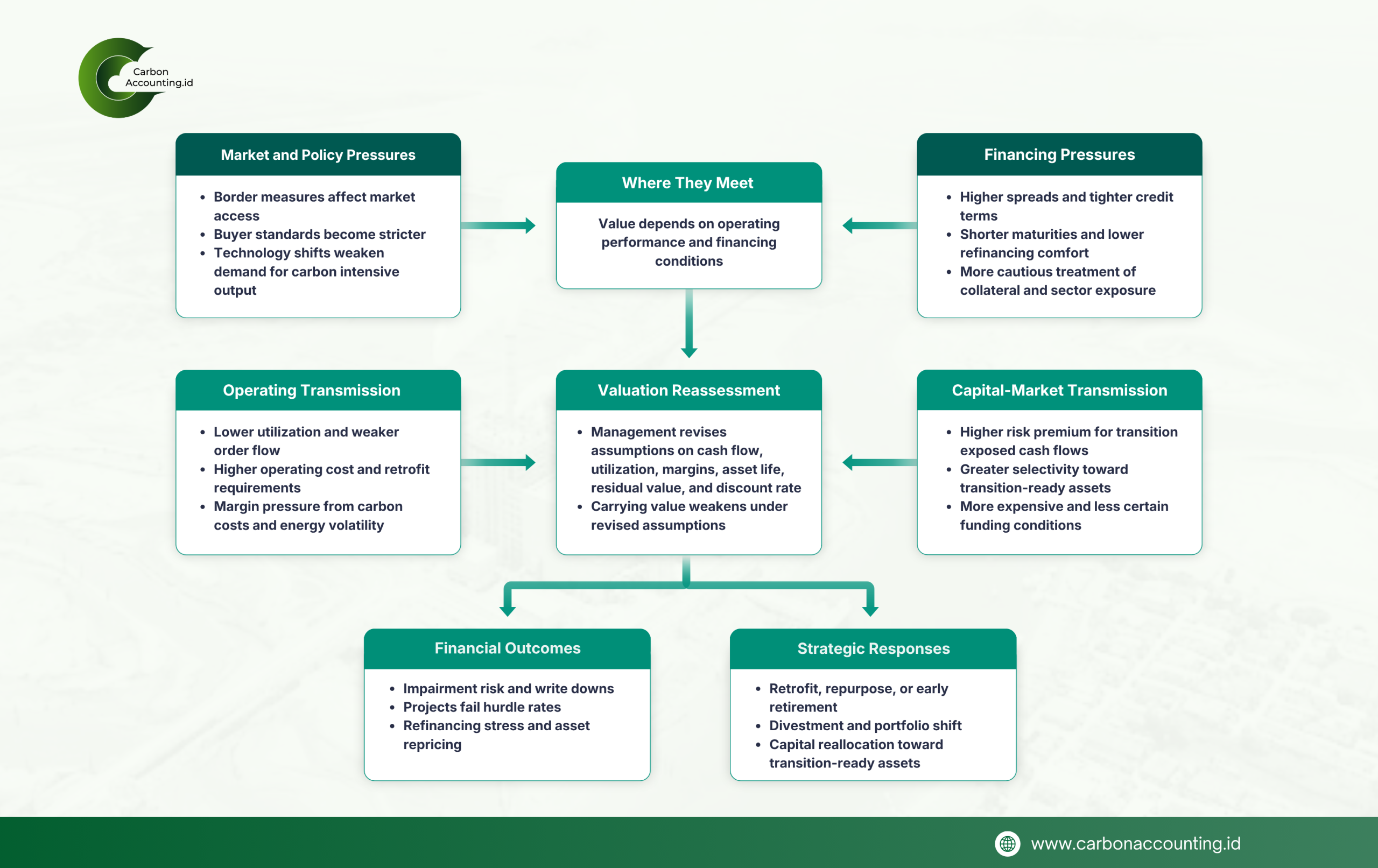

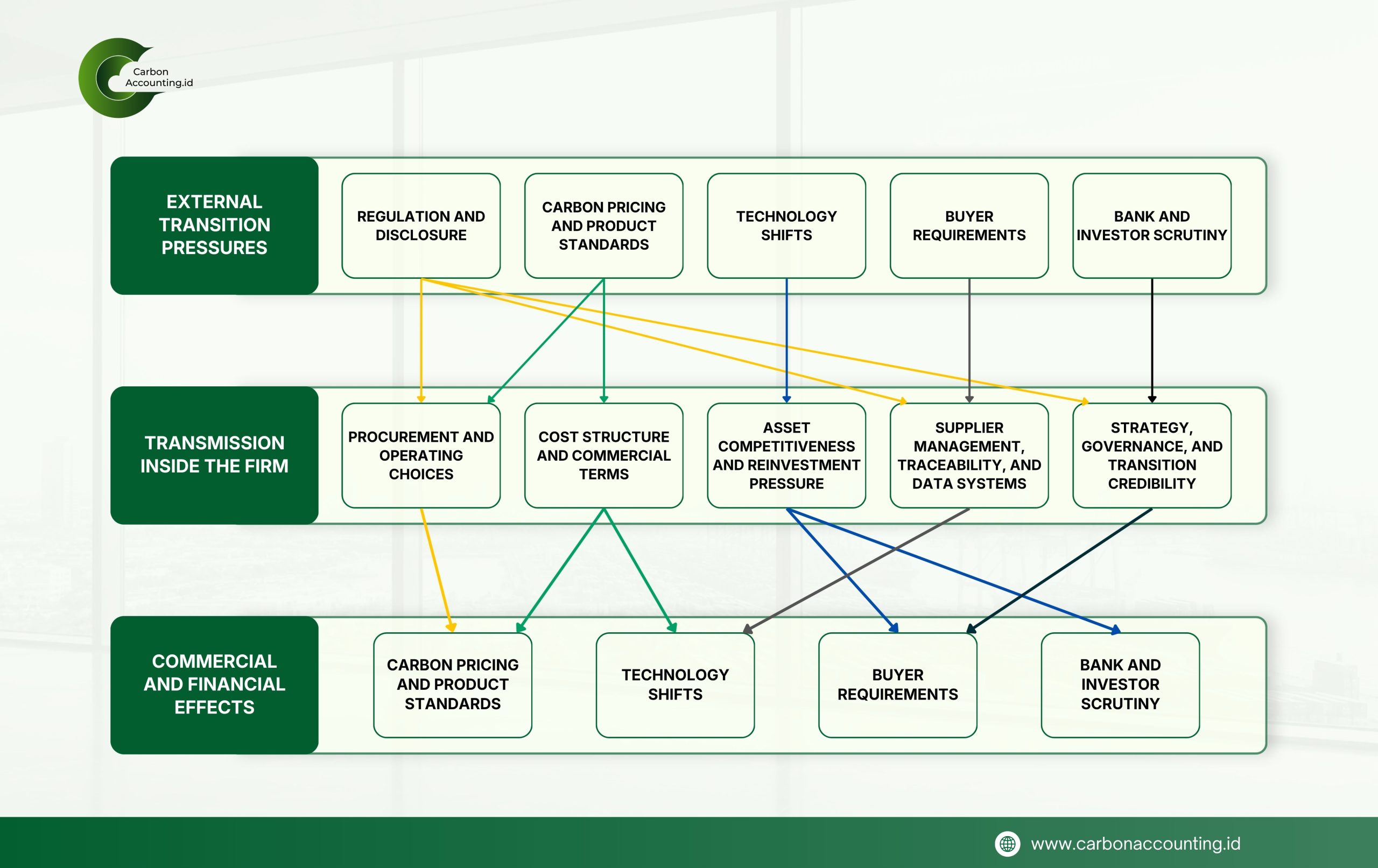

How Transition Risk Reprices High-Carbon Assets

An asset can look busy long after its value has begun to slip. That is what makes transition risk so easy to miss. The machines still run, output still leaves the gate, and the balance sheet may still treat the asset as productive. But the assumptions that once made it look secure can begin to soften much earlier.

This is the moment climate risk enters the language of finance. An asset may remain operational while it carrying value becomes harder to defend. Demand can weaken, utilization can fall, carbon related costs can rise, and the expected commercial life can shorten. The real issue is no longer whether the asset can run, but whether it can still deliver the cash flow once expected.

The pressure usually appears first in valuation assumptions. As markets begin to favour lower carbon goods, some suppliers may find themselves under pressure to provide emissions information they cannot yet produce reliably. Costs may also rise for less visible reasons, from regulatory compliance and energy price swings to insurance revisions and the need to modernize existing assets. Even resale value can weaken as the market for carbon intensive equipment narrows.

That is when impairment becomes more than an accounting term. A plant does not need to close tomorrow to face impairment today. It only needs a weaker economic future than management previously assumed. Once assumptions on margins, remaining life, exit value, or capital needs are revised, the number on the books may no longer match economic reality.

High carbon assets are especially exposed because the pressure rarely comes from one direction alone. Coal linked facilities, emissions intensive production lines, and fuel dependent transport systems can be hit by weaker market momentum, stricter buyer standards, and more expensive retrofits at the same time. What once looked viable can suddenly look fragile.

The funding side can make matters worse. Banks and investors often move before regulation fully closes in. Their caution shows up in pricier debt, shorter lending horizons, firmer terms, and growing hesitation around rollover risk and collateral value. The asset itself may still look unchanged, but its financial setting no longer does.

Seen this way, stranded asset risk is mainly an economic condition. An asset is stranded when it stops making sense in the role it was built to serve. It may still run and still face no immediate barrier to operation, but its commercial rationale has started to wear thin. The machinery remains in place, while the case for it slowly slips away.

That is the quiet lesson of transition risk. It does not wait for smoke, closure, or a legal ban to destroy value. It works by reopening assumptions and shortening the life of certainty. Delay does not save value when the basis of value is already moving. In the transition economy, waiting can become the most expensive decision of all.

{kind=link}

{kind=link}

{kind=link}

{kind=link}