Why Indonesia’s Clean Energy Projects Still Struggle to Get Built

Why Indonesia’s Clean Energy Projects Still Struggle to Get Built

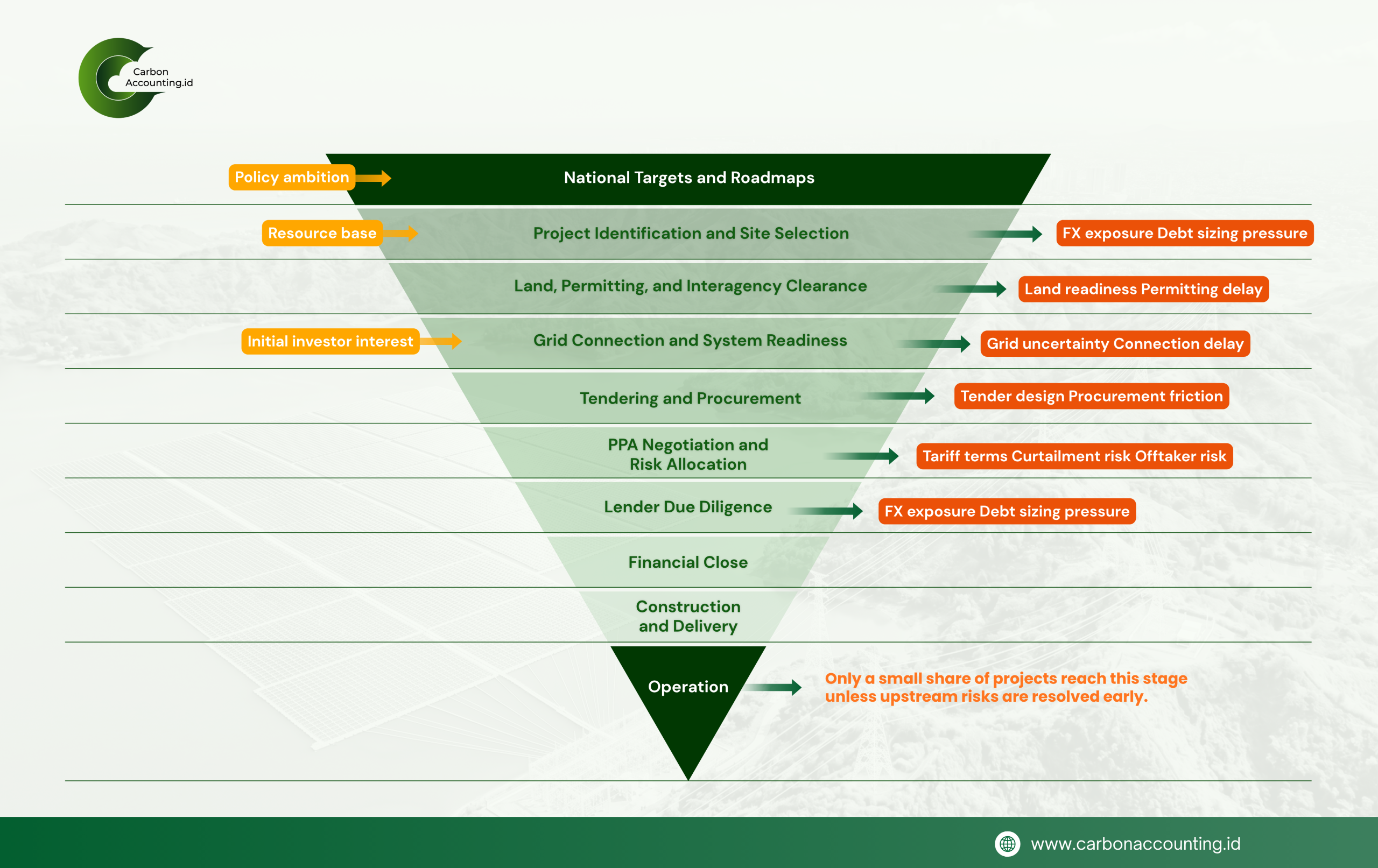

Why Clean Energy Projects Often Slow Before Construction Begins

A transition can be declared in a speech, but it is only born when the first shovel enters the ground. That is why Indonesia’s clean energy story remains unfinished. The country does not lack ambition. Too often, it lacks projects that can actually reach construction.

Clean energy is cheaper in many contexts, greener by design, and already written into national plans. Yet projects still slow down long before they become power plants. The problem is not only vision. It is whether a project can become financeable, contractable, and buildable.

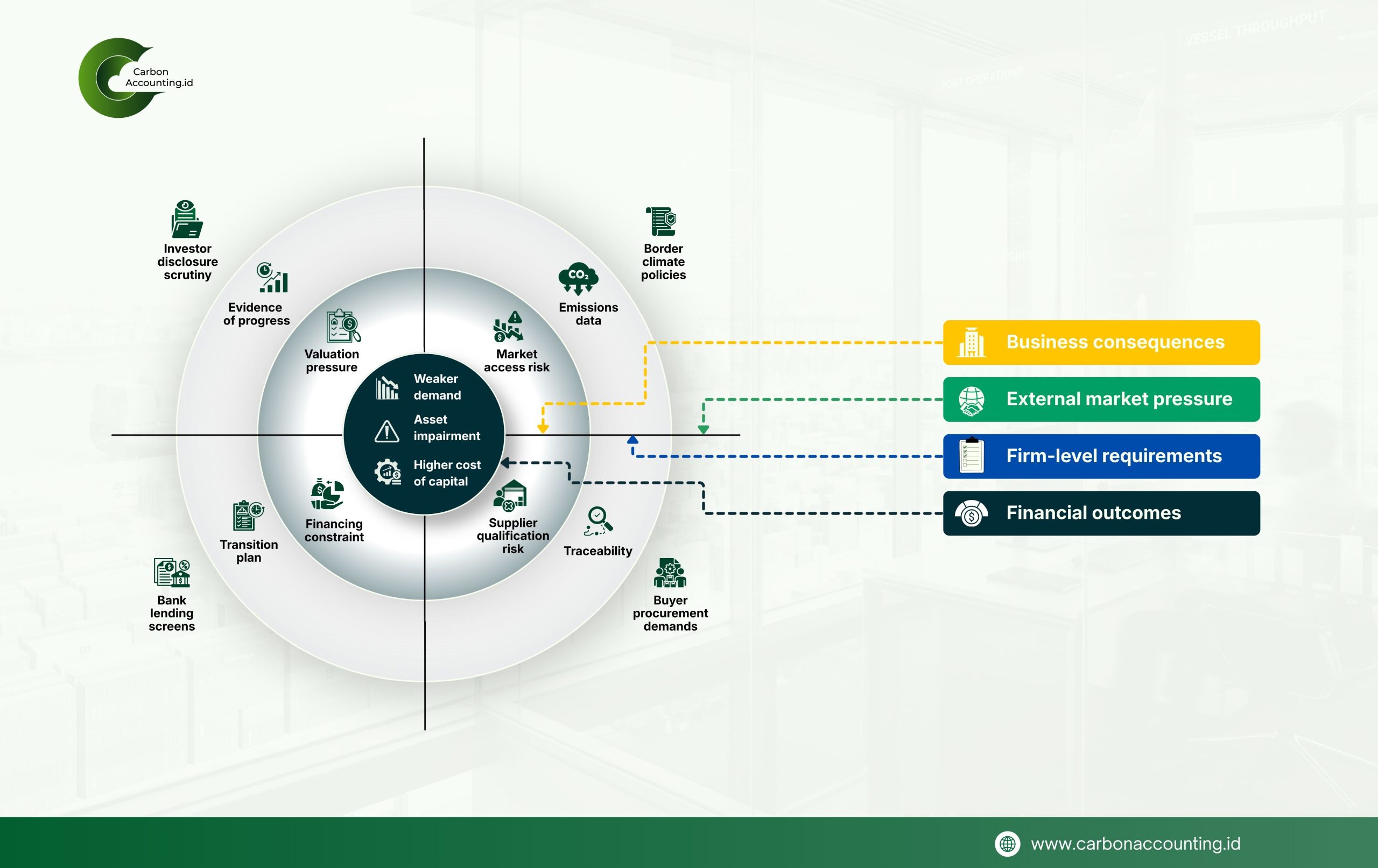

The real test is bankability. A project may look strong in presentations and planning documents, yet still lose support once lenders examine the commercial details. At that point, the question is whether the revenues are credible, the risks are clear, and the asset can operate with reasonable certainty.

That is why revenue certainty matters so much. In a single buyer system, confidence in the offtaker can shape the entire deal. Tariff design, dispatch rules, curtailment treatment, and the fine print of the Power Purchase Agreement (PPA) are not technical details at the margin. They sit at the center of whether financing moves or stalls.

Then comes the cost of risk. Renewable technology may be getting cheaper, but projects in Indonesia can still end up looking expensive once currency exposure, weak grids, and curtailment risk are taken into account. What looks efficient in a slide deck can look far less convincing in a financing model.

Permitting and procurement make the story harder. Delays often come not from poor sunlight, weak wind, or lack of geothermal potential, but from land readiness, grid connection planning, tender quality, and weak coordination across institutions. Too many projects still have to fight the same administrative battle from the beginning.

Local content policy and blended finance should be discussed without illusion. Strengthening domestic industry is important, but tight requirements can make projects more expensive when suppliers are not yet ready. Blended finance can help at the margin, but it cannot save poor project fundamentals.

That is the larger lesson. Indonesia’s clean energy problem is not mainly a shortage of resources or public ambition, but a shortage of projects that arrive at financiers in truly investable condition. In the end, the transition will be judged not by the beauty of the roadmap, but by the day the lights come on.

{kind=link}

{kind=link}

{kind=link}

{kind=link}