Why Budgets Reveal the Truth About Sustainability

Why Budgets Reveal the Truth About Sustainability

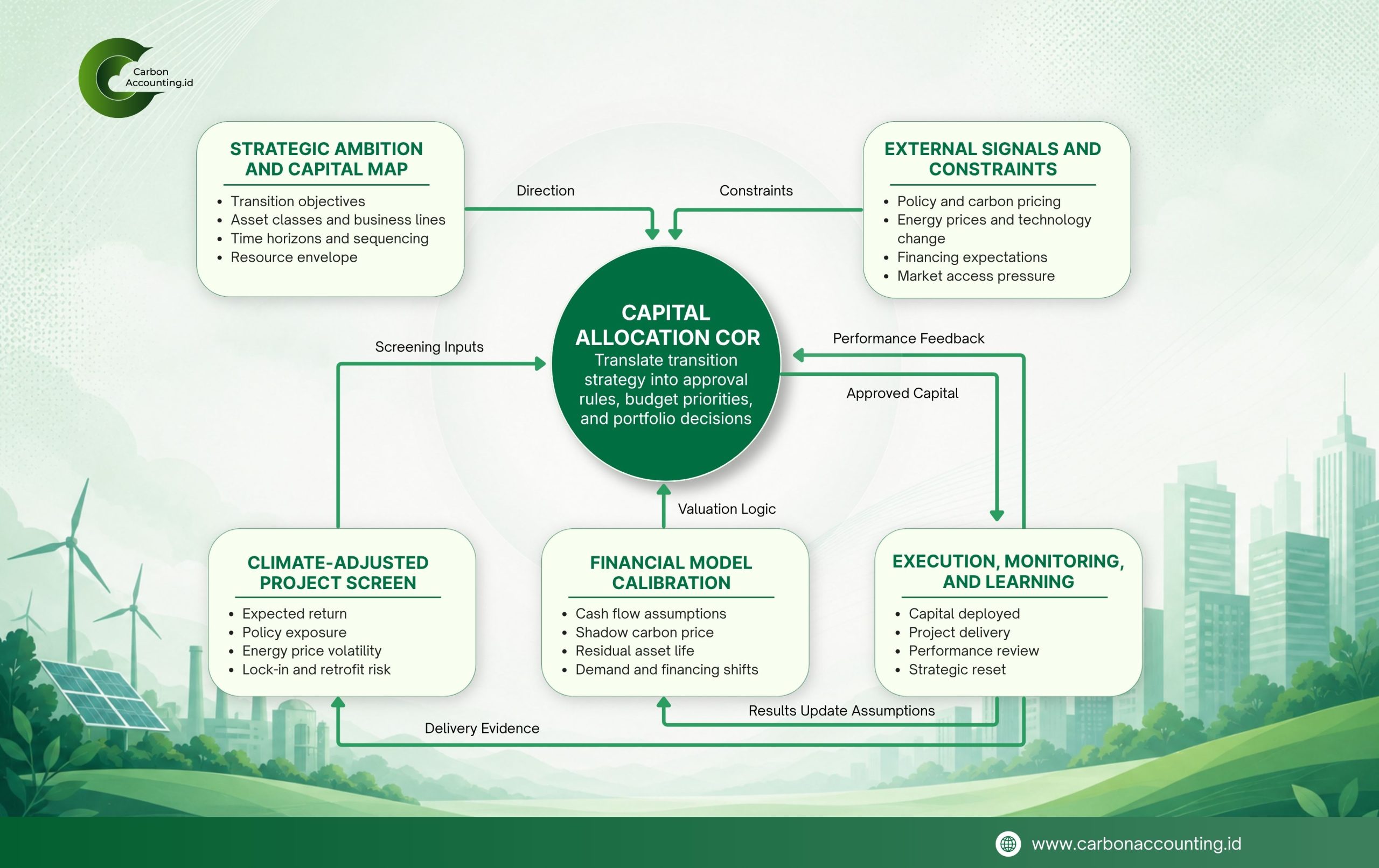

Climate-Adjusted Capital Allocation Framework

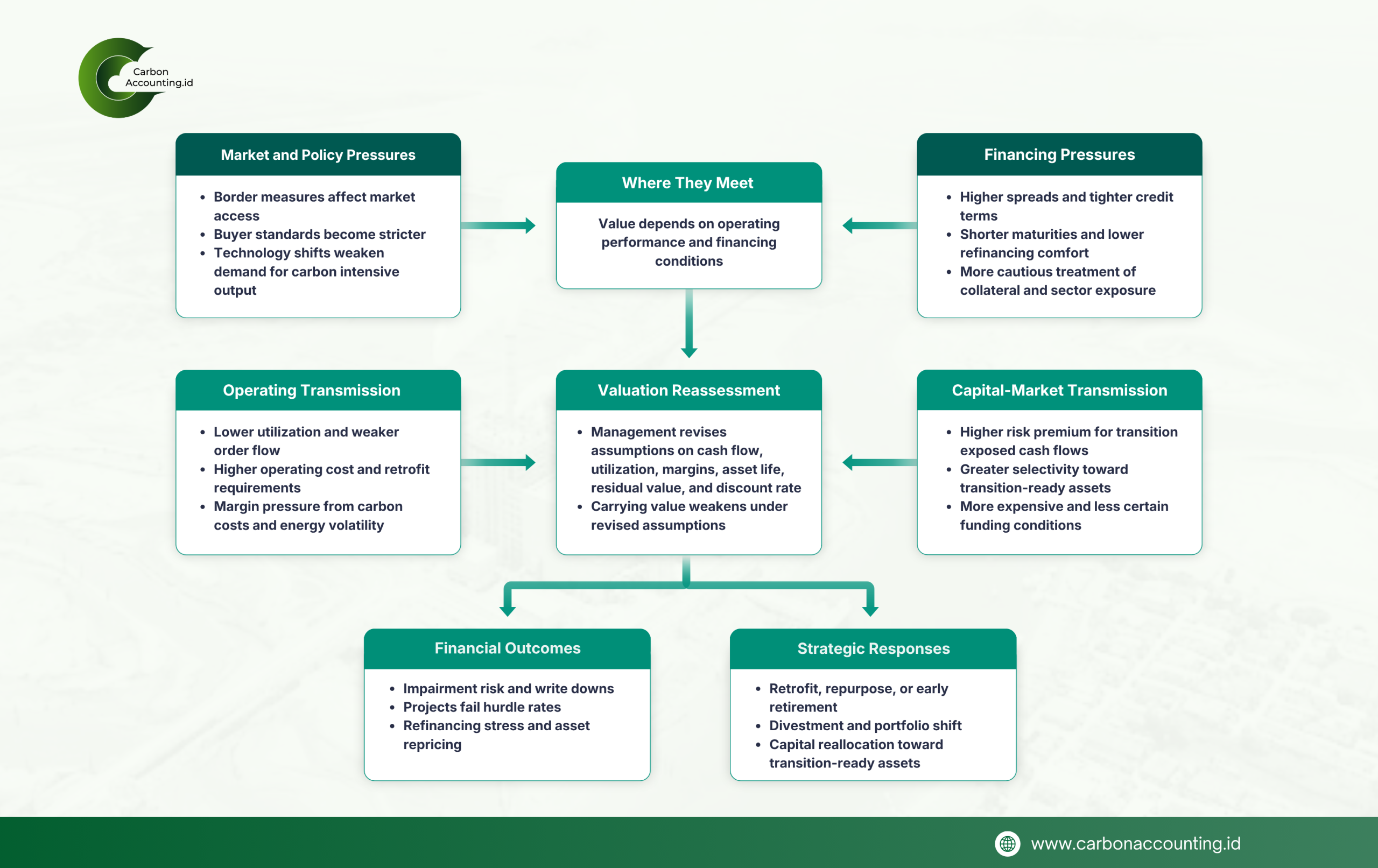

A company begins to tell the truth about sustainability when the budget is opened. Before that moment, the subject can still live safely inside speeches, targets, and polished reports.

The real test comes when management must decide what deserves capital, which costs are worth carrying, and which risks have become too expensive to ignore. In a transition era, strategy is judged less by what a company says than by what it is willing to fund.

That is why capital allocation should never sit at the edge of the sustainability conversation. It is not a finance appendix. It is the place where strategy becomes operational, because ambition must be translated into a capital map across assets, business lines, and time horizons.

In practice, that means every proposed project should face a climate adjusted investment screen. Expected return still matters, but so do policy exposure, energy price volatility, technology shifts, market pressure, retrofit risk, and the danger of locking the firm into assets that may become costly to operate or harder to finance.

This is also where internal carbon pricing becomes useful. IFRS S2 recognises both a shadow price and an internal fee. A shadow price is often the better starting point because it lets firms test project economics before regulation imposes a direct cost.

Companies also need to be careful with hurdle rates. Raising them may look prudent in uncertain times, but it can quietly eliminate projects whose value comes through lower volatility, lower compliance exposure, and a longer useful life for critical assets. A stronger approach is to improve the realism of the cash flow model itself.

That means bringing real transition variables into the numbers. Carbon cost, residual asset life, insurance burden, maintenance needs, fuel switching risk, supplier pass through, and demand shifts should be visible in the model, not hidden outside it.

A sound strategy also separates capital into different buckets. Some spending protects the current business through efficiency, resilience, and compliance. Some builds future earnings through cleaner processes, new products, digital systems, and business model redesign. Some manages exit through retirement, divestment, or capability acquisition.

From there, the discipline must carry through the whole system. Annual budgets, project approvals, and post investment reviews should all follow the same logic. If climate remains trapped in the sustainability report while capex still rewards the cheapest short-term option, the strategy will fail quietly.

In the end, budgets say what strategy really means. Targets speak in the language of aspiration, but capital speaks in the language of commitment.

{kind=link}

{kind=link}

{kind=link}

{kind=link}