Transition Risk Begins Before the Damage Is Visible

Transition Risk Begins Before the Damage Is Visible

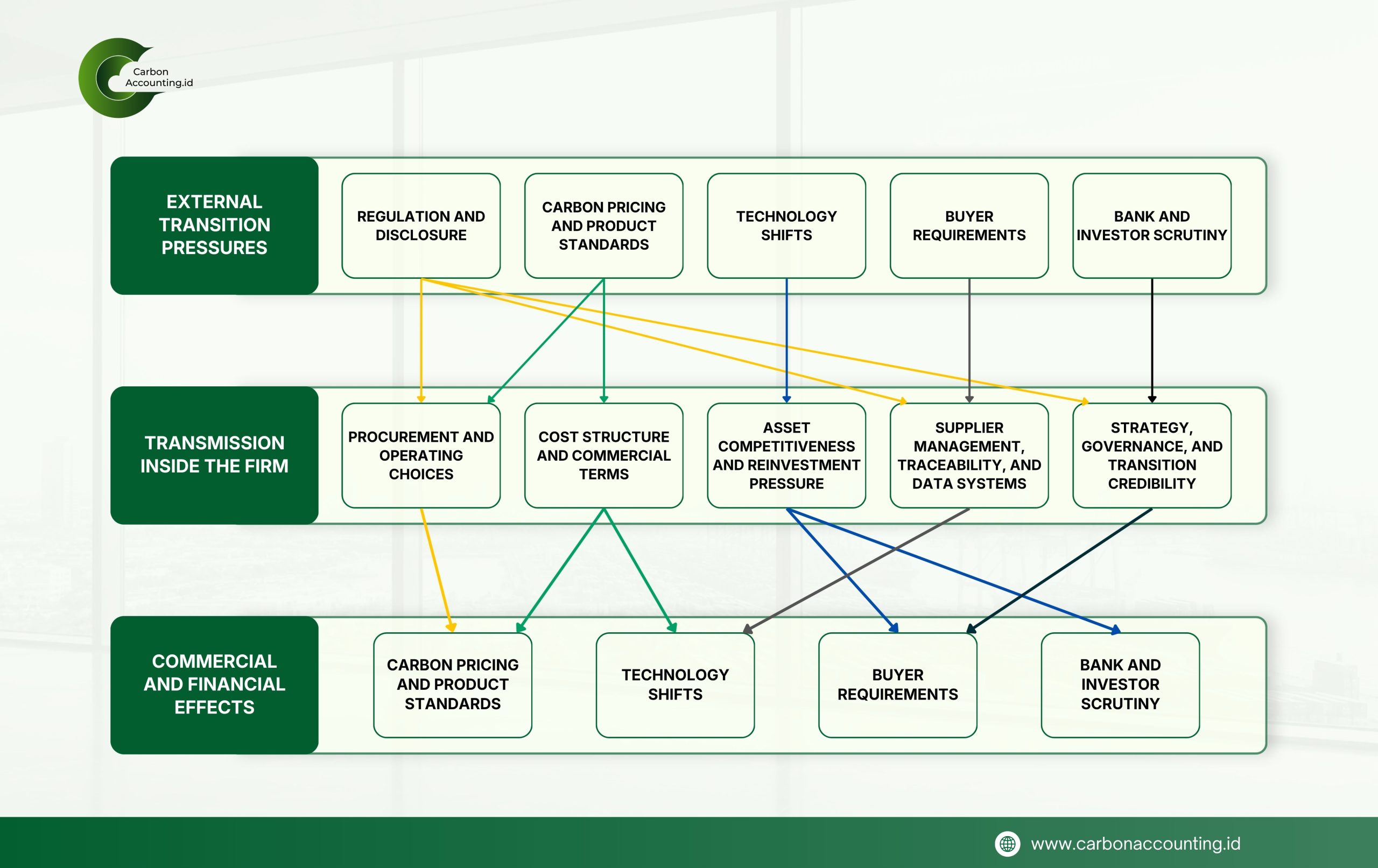

How Transition Risk Reaches the Firm

A company rarely begins to weaken only when the flood arrives. More often, the first cracks appear in quieter places, in a new rule, a tougher buyer question, a technology shift, or a lender who starts to doubt the future.

That is why transition risk matters. If physical risk enters through heat, fire, flood, or disruption beyond the fence line, transition risk enters through the economy’s response to climate change. It reshapes costs, standards, demand, and asset value before any physical damage is visible.

For too long, this risk was treated as if it belonged mainly to energy companies or other heavy emitters. That view no longer holds. As disclosure rules tighten, buyers ask for product emissions data, supply chains demand more reliable information, and financial institutions test whether business models can still endure, the pressure spreads far beyond one sector.

Regulation is often the first point of entry. What starts as a disclosure rule, a stricter product requirement, or a stronger carbon price signal does not remain in the compliance function for long. It moves into purchasing decisions, operating choices, supplier relationships, and the quality of management attention.

A second route runs through cost structure, market access, and technology. Once emissions begin to carry economic weight, production costs are no longer shaped only by labor, materials, and energy. Companies face measurement costs, adjustment costs, and sometimes the risk of losing contracts or customers. An older asset may still run, yet look increasingly expensive, inefficient, or difficult to defend.

This is where buyers, banks, and investors become decisive. Buyers want confidence that upstream emissions will not return as commercial or reputational pressure. Banks ask whether future cash flow remains credible in a changing economy. Investors want to know whether a transition plan is real or merely a story. In that moment, transition risk starts to affect financing terms, market access, and valuation.

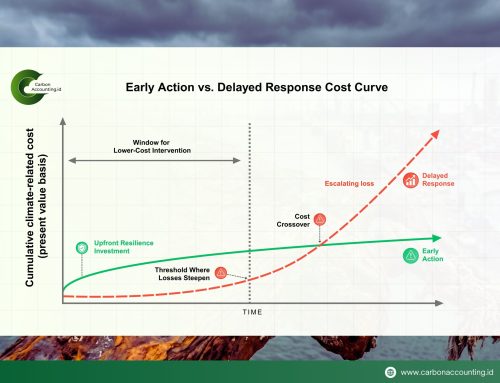

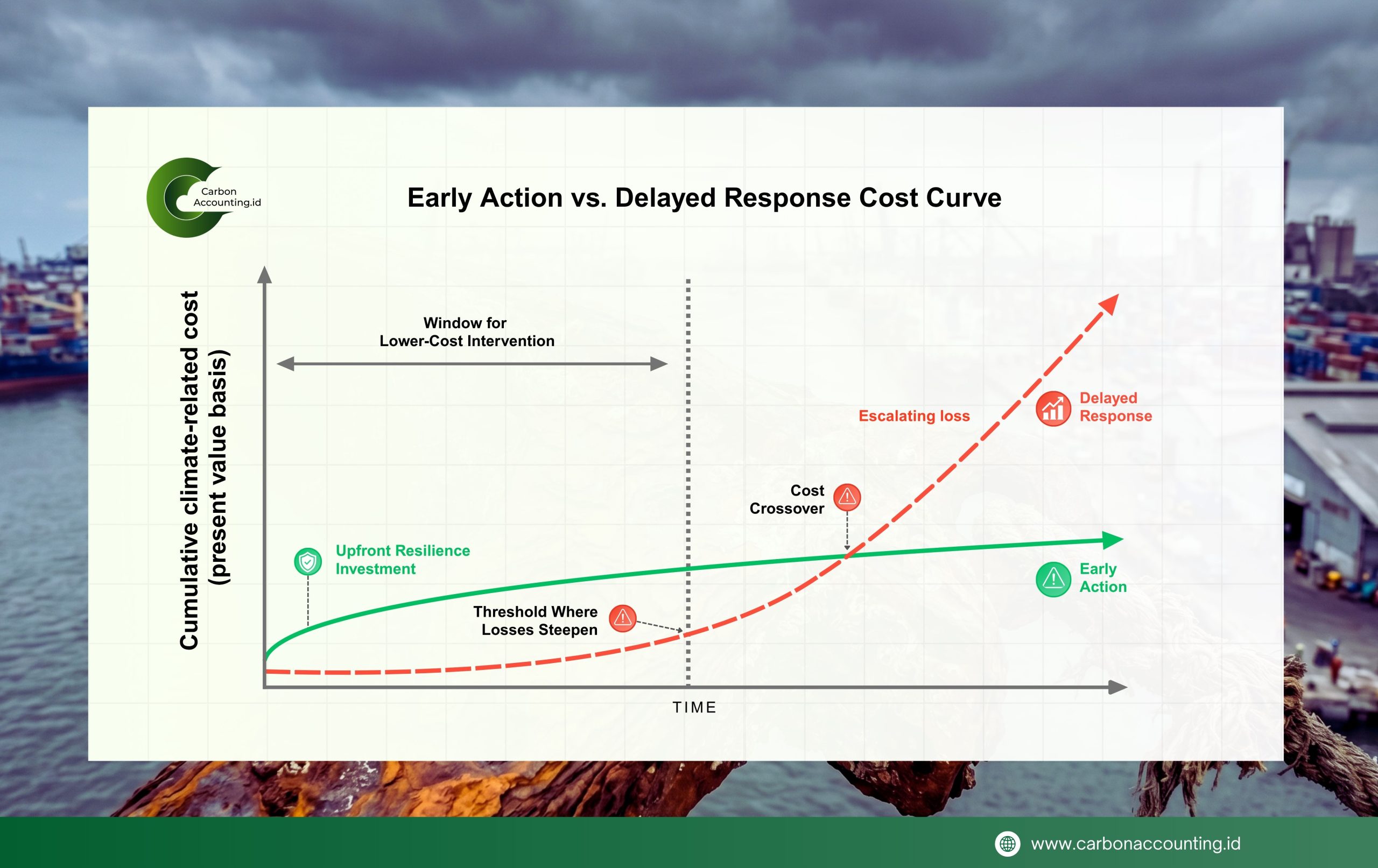

Still, this is not only a story of threat. Transition risk also separates firms that respond early from those that wait too long. Companies that move sooner usually have more room to improve data, rethink operations, and adapt on better terms.

Those that delay often change only after the damage is already visible, in lost orders, rising costs, tighter financing, or assets that no longer look secure. In a changing economy, the heaviest price is often paid not by the firm that moves, but by the firm that waits too long to see that the transition has already begun.

{kind=link}

{kind=link}

{kind=link}

{kind=link}