Voluntary and Compliance Carbon Markets in Indonesia

Voluntary and Compliance Carbon Markets in Indonesia

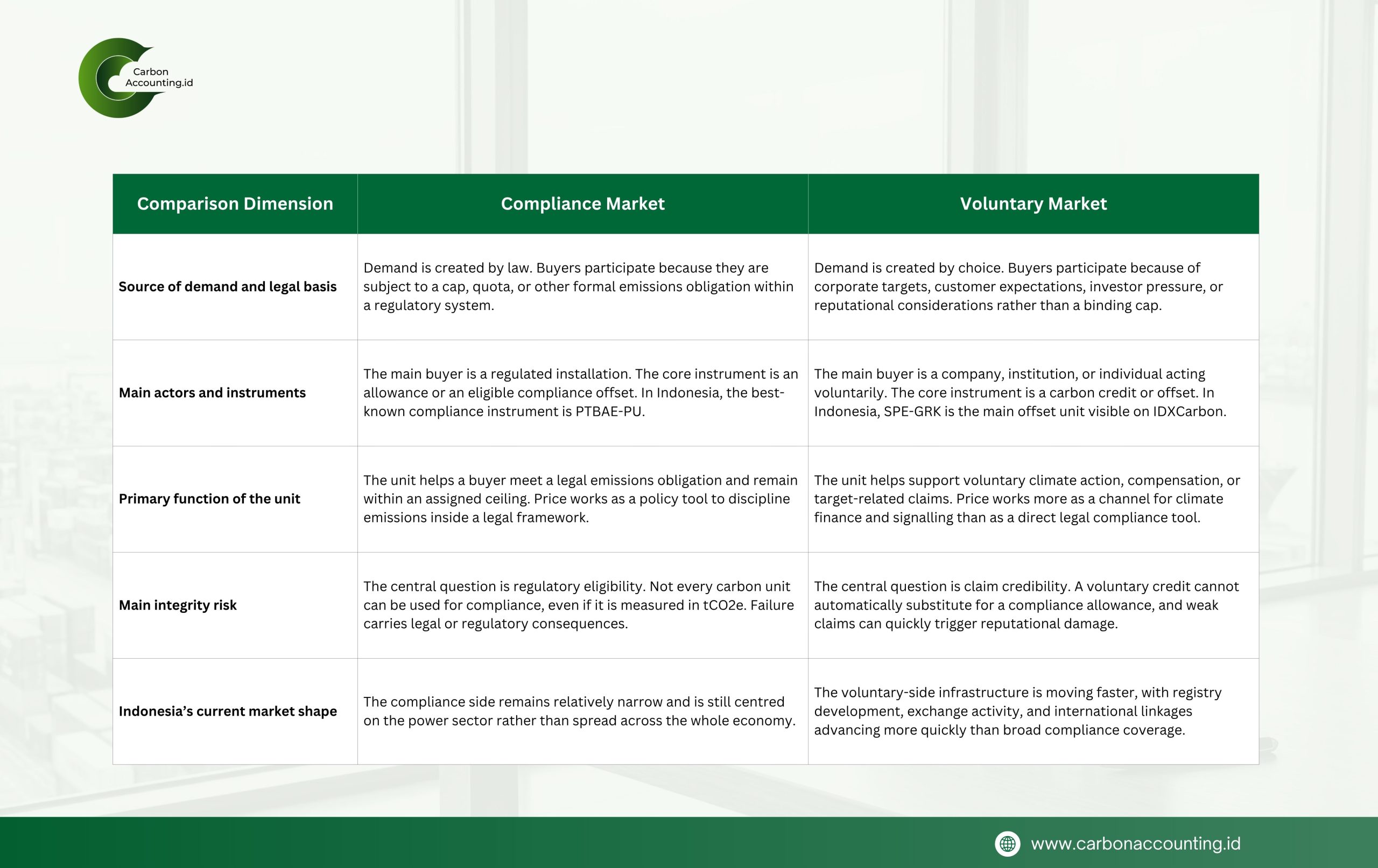

Voluntary Market vs Compliance Market: Same Unit, Different Meaning

This is where the carbon market reveals its true soul. It is far more difficult, and infinitely more fascinating, than the spreadsheets suggest. To master the divide between compliance and voluntary is to finally understand the hidden machinery of climate governance.

A compliance market exists because the law creates demand. A regulated installation must stay within an emissions limit, surrender eligible units, or face consequences. Price is meant to change behaviour inside a legal system, not simply decorate a climate narrative.

A voluntary market moves by a different force. Companies buy because of internal targets, customer scrutiny, investor pressure, or the need to protect credibility. It can bring finance to projects earlier, but it is also easier to shake when project quality or public claims begin to wobble.

That is why the two markets cannot be treated as interchangeable. A voluntary credit does not automatically do the work of a compliance allowance. A compliance unit also does not give a company a free pass to make broad climate claims. The meaning of a carbon unit depends on why it was issued, who may use it, and under what rules.

Indonesia has become clearer on this point. Presidential Regulation 110 of 2025 places carbon trading inside the wider framework of carbon economic value and states that domestic trading consists of emissions trading and emissions offsets. It also separates foreign transactions that need authorization and corresponding adjustment from those that do not.

Even so, the compliance side of Indonesia’s market is still narrow. The mandatory system remains centred on the power sector, with PTBAE-PU as the main compliance instrument. The second phase for 2025 covers about 454 generating units from 153 companies, which shows real movement, but not yet an economy wide market.

The voluntary side is moving faster in market infrastructure. Indonesia launched its first international trading of carbon units through IDXCarbon on 20 January 2025, has strengthened SRN PPI, and has expanded mutual recognition arrangements with Verra, Gold Standard, Global Carbon Council, and Plan Vivo. As of 4 April 2026, IDXCarbon shows more than 1.9 million tCO2e traded, value above IDR 93.7 billion, 10 listed SPE-GRK projects, and 153 participants.

This distinction matters because markets do not fail only when prices are weak. They also fail when units lose meaning. Indonesia does not only need more carbon transactions. It needs each unit to say exactly what it can do, and nothing more.

{kind=link}

{kind=link}

{kind=link}

{kind=link}