ISSB-Based Disclosure and the Road to 2027

ISSB-Based Disclosure and the Road to 2027

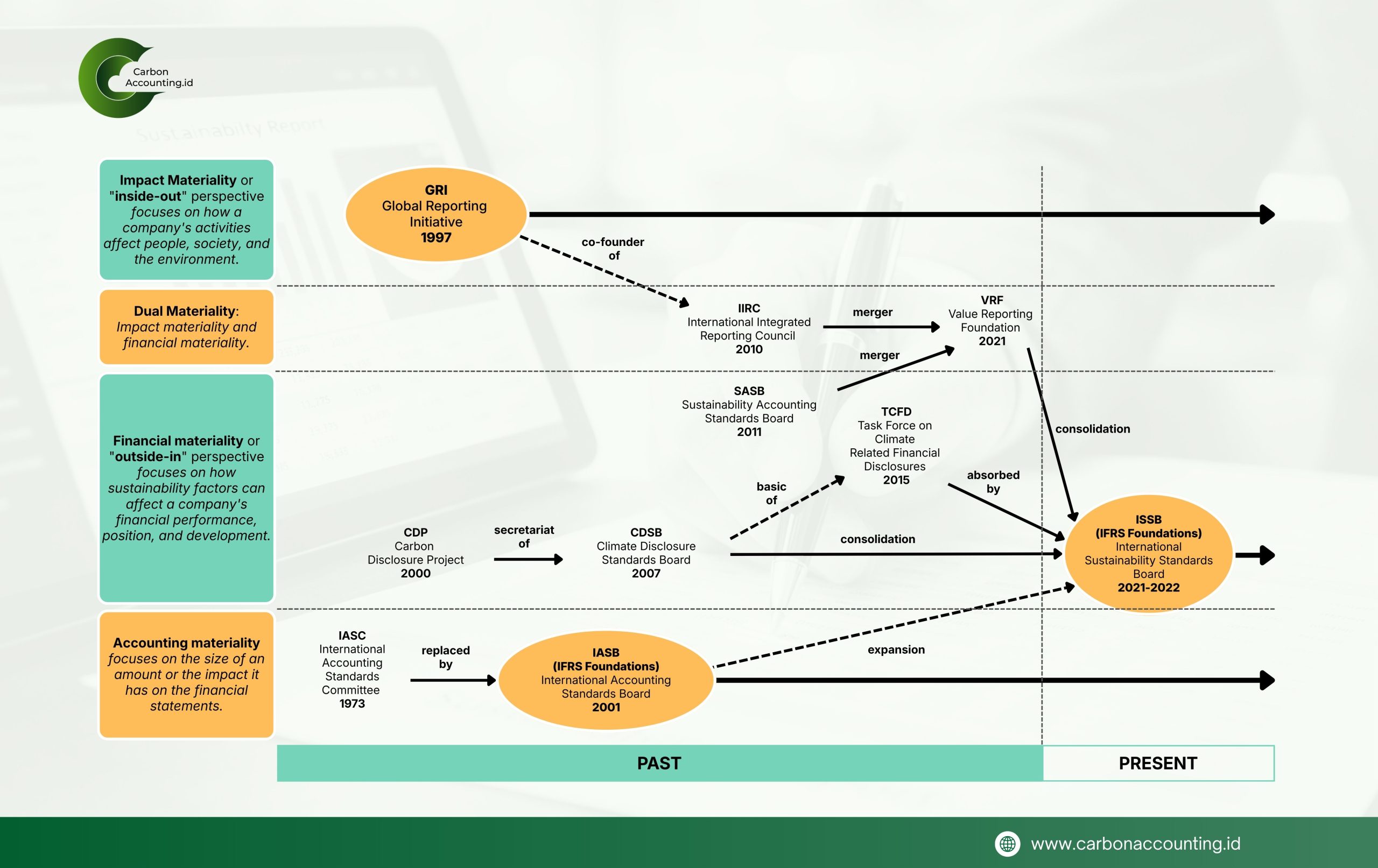

Evolution of Corporate Reporting.

Mature sustainability no longer relies on beautiful words. It begins to be measured by information that can be tested, compared, and used to read a company’s future.

That is why the ISSB global baseline matters for Indonesia. Through PSPK 1 and PSPK 2, ratified by DSK IAI on July 1, 2025, Indonesia translated IFRS S1 and IFRS S2 into the national reporting language, with an effective date of January 1, 2027, and early adoption permitted.

This shift is not merely about changing the format of a report. PSPK 1 sets the general requirements for sustainability related financial disclosures, while PSPK 2 focuses specifically on climate related disclosures. Together, they bring reporting closer to the logic already shaping capital markets and financial decision making.

At the center of this architecture are four: governance, strategy, risk management, and metrics and targets. These pillars ask a harder question than many sustainability reports asked in the past. They ask not only what a company says it cares about, but how climate and other sustainability issues are governed, managed, and linked to performance.

The most important change lies in materiality. The emphasis is no longer on producing a sustainability story that sounds convincing. It is on identifying risks and opportunities that could reasonably affect enterprise value, including cash flow, access to finance, and the cost of capital.

For issuers, banks, and state-owned enterprises, the road to 2027 means rebuilding internal discipline. Boards and commissioners need to treat sustainability as a governance and risk issue. Finance, sustainability, operations, legal, and risk teams can no longer work in separate lanes if disclosures are to be consistent, decision useful, and credible.

This also changes the role of consultants and assurance providers. The market will need more than report writers. It will need translators of standards, architects of process, testers of controls, and independent professionals who can assess whether the underlying data, assumptions, and claims are truly robust.

In the end, the greatest test may be the company’s data system. Without clean structures, documented evidence, clear methodologies, and disciplined review processes, even the best intentions will struggle to become reliable disclosure. The road to 2027 is not simply a road to compliance. It is a road to a new discipline, where sustainability no longer stands at the edge of business but moves into the heart of corporate decision making.

{kind=link}

{kind=link}

{kind=link}

{kind=link}